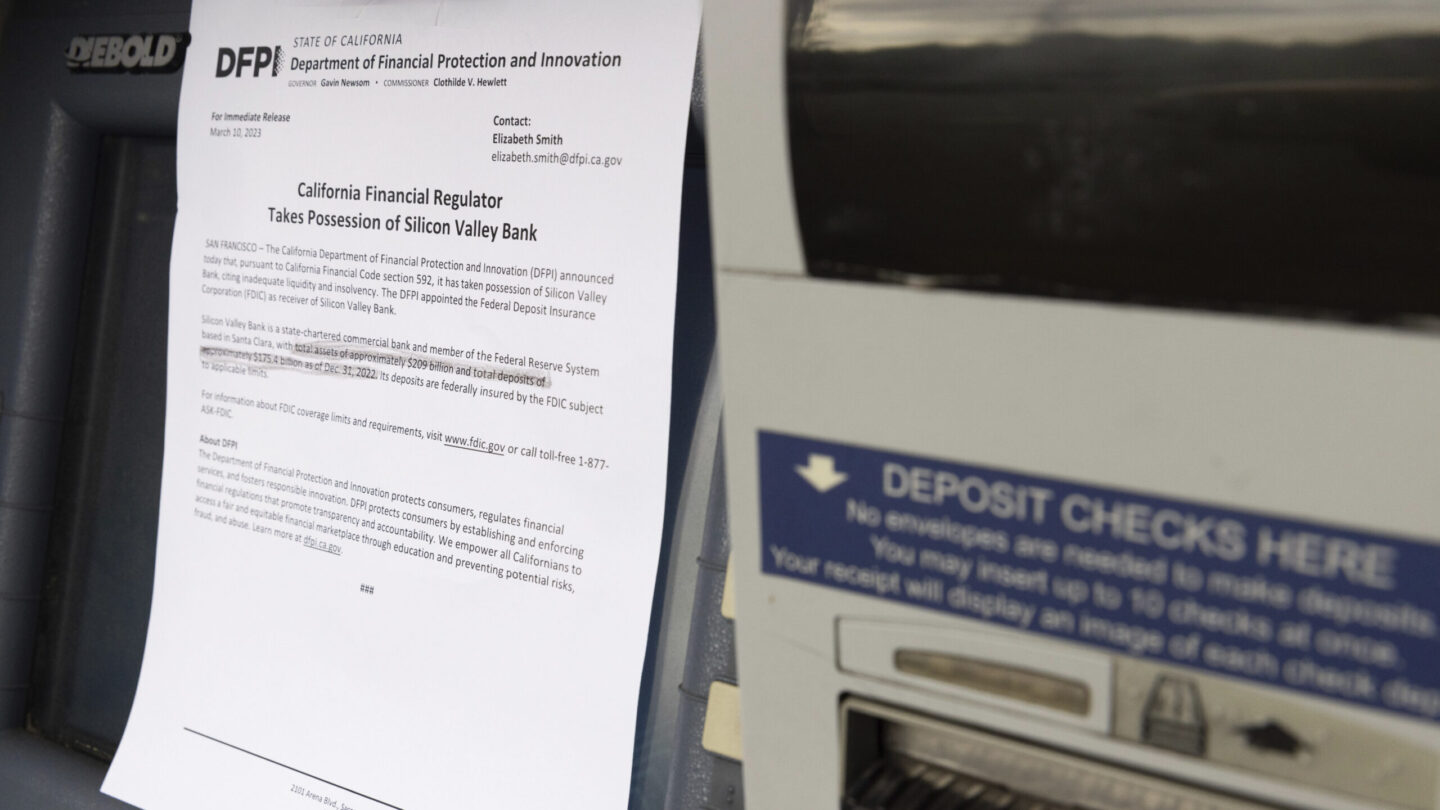

The news about bank collapses and emergency rescues can seem both alarming and distant.

Maybe you wondered: is my bank account safe? If it’s under $250,000, your money is fully insured by federal authorities under all circumstances.

So you might ask: why should I care about the knotty problems of the banking world? It’s a reasonable question.

There are possible consequences for the U.S. economy, small business and regular people. Here are some of them.

Will this trigger a recession?

That depends on many factors.

Will banks get more cautious about lending? This would mean less access to money for real estate development, business expansions and purchases of homes and cars. Experts at Goldman Sachs said that smaller banks in particular may tighten up, resulting in slower economic growth for the nation as a whole.

People who control budgets of families and businesses hold sway, too. Will employers get leery about hiring new workers? Will shoppers cool their travel plans or delay big purchases? These expenditures are key pillars of the U.S. economy and a big scale back would bite.

And what happens to the banking system? Experts point to a handful of regional banks that took similar risks to the failed lenders and could be in danger. The Federal Reserve is offering funding to help shore up banks’ cash reserves and avoid another damaging bank run. But the Fed is also expected to raise interest rates in its long-term quest to fight inflation.

Will getting a loan become even more expensive?

Possibly, and it’s a similar explanation.

On Wednesday, the Federal Reserve will say which path it chooses: to raise interest rates again and keep tightening the screws on inflation or to pause for a gift of a breather to the banking system.

Interest rates, which guide how much people and businesses pay for various loans, have already been rising for over a year.

Now, the question is whether banks may also get more conservative and reduce how many loans they issue. They might decide this because of general belt-tightening in an uncertain economy – or if they face tougher regulations in the fallout of recent bank failures.

Will the federal rescue trickle down to higher fees for regular bank customers?

Here’s the context. To prevent wider panic, the Federal Deposit Insurance Corp. broke with normal policy to guarantee that all customers could get their money back from the collapsed SVB and Signature Bank. The call was remarkable because over 90% of SVB’s and nearly 90% of Signature’s deposits exceeded the $250,000 cap for FDIC insurance.

That insurance money came from a fund pooled through quarterly fees from FDIC-insured banks. With billions of this rainy-day fund now spent, how will it get replenished?

This depends on how successful the FDIC will be in selling the failed banks’ assets. It also depends on the steadiness of the banking system: A cascade of similar insurance payouts could mean the FDIC might assess higher fees on banks, who could then pass on the new costs to all their customers.

Could this make big banks even more powerful?

Emotions and perceptions can be powerful drivers. And the government’s swift financial rescue may create the unintended perception that in an emergency, customers at big-enough banks will get bailed out no matter what – whether their deposits are insured or not.

This could mean bankers who manage uninsured accounts above the $250,000 cap may start taking greater risks, or the people who own those accounts may scrutinize their bankers’ decisions less.

Another worry is a potential exodus from smaller, regional banks to bigger ones — based on that perception of less risk (even though there’s no indication that small banks are in trouble).

This could force smaller banks to close or get absorbed into bigger institutions, possibly leaving fewer lenders commanding more clout.

Does this mean a new era of less Silicon Valley innovation?

Before its collapse, Silicon Valley Bank was a key player in the startup ecosystem, facilitating meetings of entrepreneurs and venture-capital investors in addition to holding their accounts and loans. It did business with nearly half of U.S. tech startups, including those doing biomedical research.

“It removes a capital source for many companies … and it also means that some companies may end up failing,” Rob Chess, chairman of Nektar Therapeutics, told KQED’s Lesley McClurg.

The failures of SVB and New York’s Signature Bank, which was big on cryptocurrencies as well as tech, may lead to a slowdown in lending to smaller, untested business ventures – or a slowdown in Silicon Valley’s startup spending overall.

NPR’s Stacey Vanek Smith, Scott Horsley, Arezou Rezvani, Bobby Allyn and David Gura contributed to this report.

Copyright 2023 NPR. To see more, visit https://www.npr.org.

9(MDAxODM0MDY4MDEyMTY4NDA3MzI3YjkzMw004))